⚡ Introduction: Why Australia’s Battery Capacity Matters

Australia sits at a decisive moment in the global battery supply chain. The nation is already a world leader in lithium, nickel and graphite, but it remains an emerging player in actual battery cell manufacturing.

As EV sales rise worldwide, markets are demanding secure, ethical and sustainable sources of both raw materials and finished lithium-ion batteries. This is where Australia sees its opportunity—leveraging local resources, clean-energy potential and technology partnerships to move further down the value chain.

🔍 Key Points at a Glance

| Key Insight | Summary |

|---|---|

| Resource Advantage | Australia has some of the world’s largest lithium, nickel and graphite reserves. |

| Early Manufacturing Stage | Domestic cell output remains small; most minerals are still exported for processing. |

| Growing Policy Support | Federal and state initiatives aim to build a competitive, sustainable battery sector. |

| 2030 Scenarios | Capacity could reach 0.5–40+ GWh/year, depending on investment and execution. |

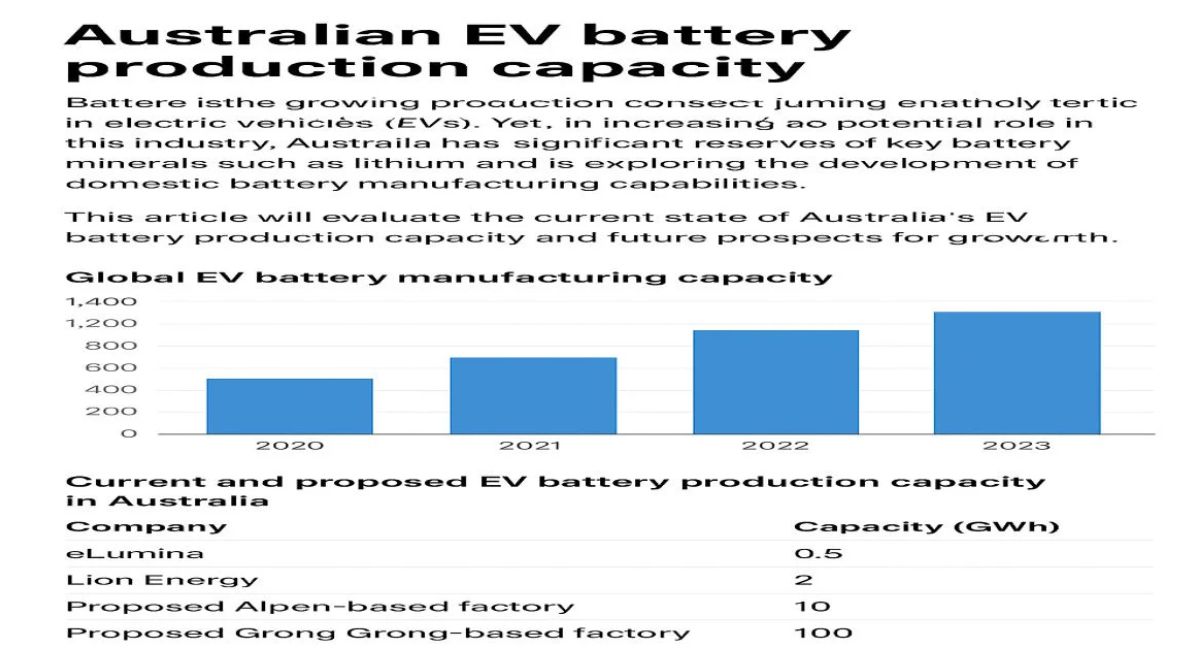

📊 Snapshot: Current Australian EV Battery Production Capacity (2024–2025)

Australia’s EV battery manufacturing sector is still in early development. As of late 2025, the landscape consists of pilot lines, small-scale pack assemblers and several proposed gigafactory projects.

Current Representative Projects

| Project / Company | Location | Stage (2025) | Estimated Capacity | Notes |

|---|---|---|---|---|

| eLumina Battery & EV Charger Factory | Australia | Operational | ~300 units/year | Focus on R&D, workforce training, small-scale production |

| Announced “First Australian Gigafactory” (multiple proponents) | VIC, NSW, SA | Planning | 2–30 GWh (various proposals) | Many are still in early funding or design phases |

| Regional Recycling & Storage Projects | NSW, WA | Under development | Modular capacity | Supports circular economy and future feedstock |

Note: Capacity values fluctuate as projects progress.

🏗 Major Players: What’s Real and What’s Aspirational?

Australia’s battery ambitions involve four main stakeholder groups:

| Type of Player | Description |

|---|---|

| Startups & SMEs | Building pilot cell lines, components (anodes, cathodes, electrolytes), and battery packs. |

| Mining Companies | Moving downstream by investing in lithium conversion, cathode precursor plants and battery materials. |

| International Partners | OEMs and global manufacturers exploring joint ventures in Australia. |

| Government-led Consortia | Funding projects that support sovereign manufacturing capability. |

The challenge for industry observers is distinguishing genuine progress (funded projects, equipment orders, site approvals) from aspirational press releases or early memorandums of understanding (MOUs).

🔬 Technology Choices & Manufacturing Models

Australian battery development is likely to take a staged pathway rather than jumping directly to 50 GWh gigafactories.

Expected Technology Areas of Focus

| Category | Likely Australian Emphasis | Reason |

|---|---|---|

| Cell Chemistries | LFP, NMC | Suited to EVs and stationary storage |

| Active Materials | Cathode active material (CAM), anode materials | Lower-risk entry to downstream value chain |

| Recycling | Lithium, cobalt, nickel recovery | Secures domestic raw material loop |

| Cell-to-Pack Integration | EV and storage system assembly | High demand in domestic market |

A realistic national strategy includes:

refining → precursor materials → pilot lines → gigafactory scale-up

💰 Economic & Policy Drivers

Government Support

Australia has introduced several incentives for clean manufacturing, including:

-

Critical Minerals Strategy

-

Federal grants for renewable-energy manufacturing

-

State-based industry development funds

-

Fast-tracked approvals for low-emissions industrial precincts

Market Demand

While Australia’s domestic EV market is smaller than Europe, China or the US, the country is well-placed to become a regional export hub.

Investment Realities

A single gigafactory can cost AUD $1–3+ billion. Access to stable financing and OEM offtake agreements will decide which projects advance.

🔧 Supply Chain & Technical Challenges

| Challenge | Explanation |

|---|---|

| Chemical Conversion Capacity | Australia’s lithium hydroxide plants are expanding but remain constrained. |

| Electrode Production | Requires precision equipment and chemical engineering expertise. |

| Equipment Lead Times | Cell manufacturing tools often have 12–24 month delivery windows. |

| Skilled Workforce | Electrochemical engineering talent is still limited. |

| Energy Footprint | Manufacturers need access to reliable, low-carbon electricity. |

Australia must coordinate industry, research and government efforts to overcome these barriers.

🌱 Environmental & ESG Considerations

Local battery manufacturing must ensure:

-

Efficient water usage

-

High worker safety standards

-

Clean-energy powered production

-

Transparent environmental reporting

-

Integrated recycling systems

Recycling, in particular, will reduce reliance on virgin mining and improve the environmental footprint of the domestic EV supply chain.

📈 Australia’s EV Battery Capacity Scenarios to 2030

Below are three realistic trajectories based on investment, policy support and export opportunities.

| Scenario | Estimated 2030 Capacity | Key Drivers |

|---|---|---|

| Conservative | 0.5–2 GWh/year | Slow growth, pilot projects only |

| Moderate | 5–15 GWh/year | Several successful scale-ups, stable funding |

| Ambitious | 20–40+ GWh/year | Fully commissioned gigafactories and integrated supply chains |

Reaching the ambitious scenario would position Australia as a major regional supplier.

📚 Case Studies (Short Highlights)

1. eLumina

A small but important step in localising skills, research and early battery production.

2. Regional Recycling Projects

Facilities in NSW and WA aim to recover lithium, nickel and cobalt from waste batteries, helping Australia build circular supply chains.

3. Overseas-Linked Investments

Some Australian companies are co-investing in offshore plants in Southeast Asia, ensuring access to large-scale manufacturing while supplying Australian markets.

🧭 Practical Recommendations for Policy Makers & Industry

| Priority | Action |

|---|---|

| Build Integrated Value Chains | Link mining → conversion → precursor → cell → pack. |

| De-risk Gigafactory Investment | Use blended finance models. |

| Grow Local Skills | Expand TAFE and university electrochemistry programs. |

| Power with Renewables | Reduce lifecycle emissions for global competitiveness. |

| Expand Recycling | Support collection and local black-mass refining. |

| Communicate Realistically | Distinguish between MOUs and committed investments. |

📌 Roadmap Checklist for Developers & Investors

| Phase | Key Activities | Typical Timeline |

|---|---|---|

| Feasibility & Site Selection | Environmental studies, grid/water assessments | 6–18 months |

| Pilot Line Installation | Testing chemistries and training staff | 12–36 months |

| Financing & Procurement | Secure capital, order equipment | 12–24 months |

| Construction & Commissioning | Build facilities and safety systems | 12–24 months |

| Commercial Operation | Ramp to stable capacity | 6–24 months |

❓ Frequently Asked Questions

Q1: Does Australia have operational gigafactories?

Not yet. Most projects are pilot lines or proposals as of 2025.

Q2: Will domestic battery production reduce EV prices?

Potentially, but cost savings depend on scale, renewable-power access and automation.

Q3: What chemistries will dominate in Australia?

LFP for stationary storage and affordable EVs; NMC for high-performance automotive uses.

🏁 Conclusion

Australia has a rare chance to evolve from a raw-materials exporter into a global clean-energy manufacturing hub. With strong resource advantages, emerging technology capabilities and supportive government policy, the country can build a competitive EV battery industry.

Success, however, requires strategic investment, skilled workforce development and realistic execution. If these pillars align, Australia could achieve multi-gigawatt battery production by 2030 and play a major role in the Asia-Pacific clean-energy economy.

1 thought on “Australian EV Battery Production Capacity”